HSA excess contribution still showing after removal of excess contribution

Hi, hoping to get some help with an HSA situation.

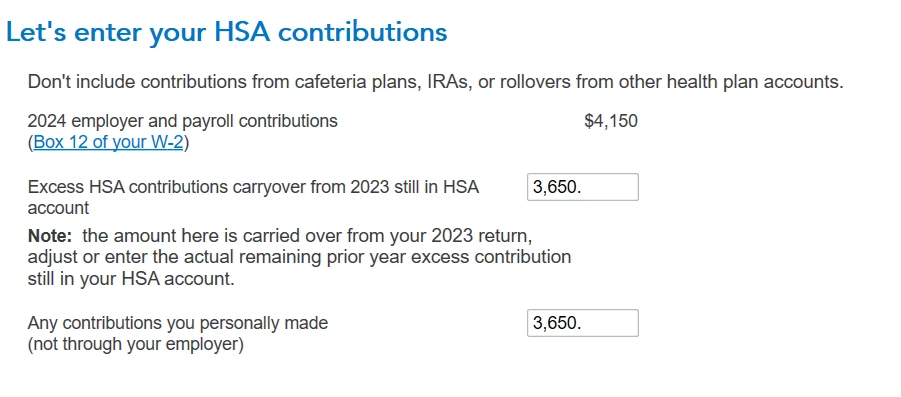

In 2022/2023, I made the maximum contributions to my HSA ($3650/$3850) via employer contributions.

In early 2024, I learned that those contributions were ineligible. I removed the 2023 contributions before Tax Day and amended my 2022 return to reflect the excess. So for my 2022 and 2023 returns, I had $3650 excess.

By the time I realized this, I'd already contributed to my HSA for 2024, which I was eligible for ($4150). I then distributed $3650 worth of 2024 contributions as excess.

In summary, I have the following for 2024:

- $3650 excess carried over from 2022 -> 2023

- $7500 = $3850 (from 2023) + $3650 (from 2024) of returned excess contributions

- $4150 of new employer contributions

So my net contribution for 2024 should be only $4150.

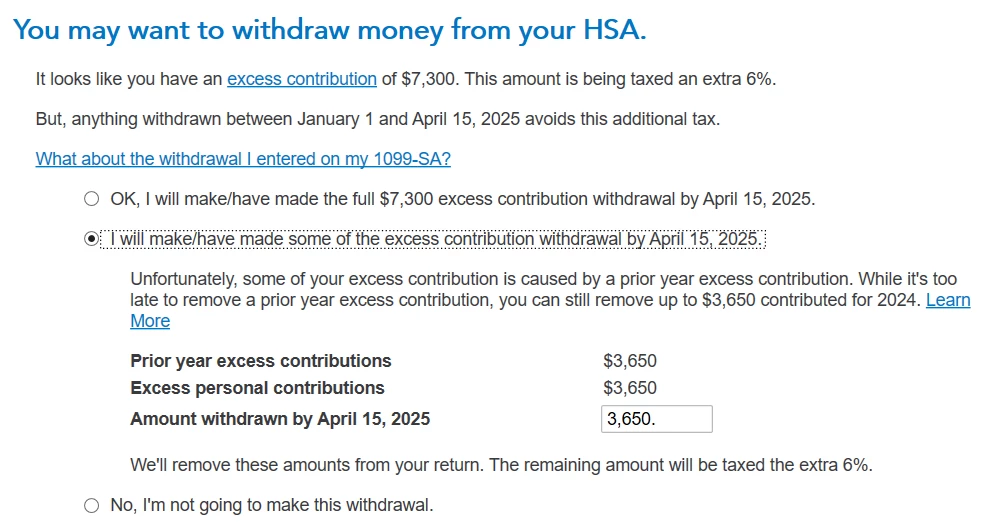

When I try to enter my 1099-SA, it still shows that I have a carried-over balance. Looking at Forms 5329 and 8889, the excess contribution hasn't affected either the $4150 new contributions or the $3650 carryover, nor is there any tax levied on the returned excesses.

My 1099-SA has a distribution code of 2 (box 3).

How can I set the forms to correctly reflect that the return of excess should balance out the contributions?

Thanks in advance.