Steam Train

When you received 1099-B for your brokered CDs, what did you enter for the "Description" on form 8949? I am new to this so I have no idea how to enter brokered CDs description on form 8949. Can you show me some examples? Also, did you enter the dates you bought and sold/redemption?

I didn't enter them myself...the file imported OK from Fidelity directly into the forms 1099-B/8949. So all I did was check that the term (short-term or long term...but all were long term for me) and zero gain was noted i.e. Purchase price and Redemption price was the same.

________

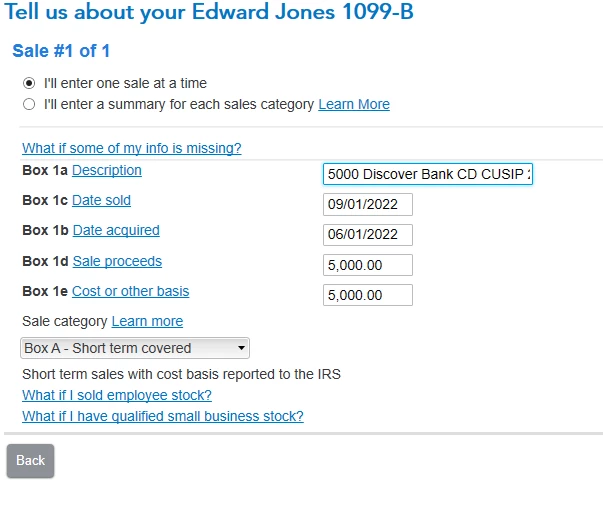

I'm not an expert but, in my Desktop software, based on what I saw was reported in my 8949 for those years....for a manual entry it would likely look like this (There was a CUSIP number in the 1099-B for each, and I included that in my description, but don't know if it's necessary).: