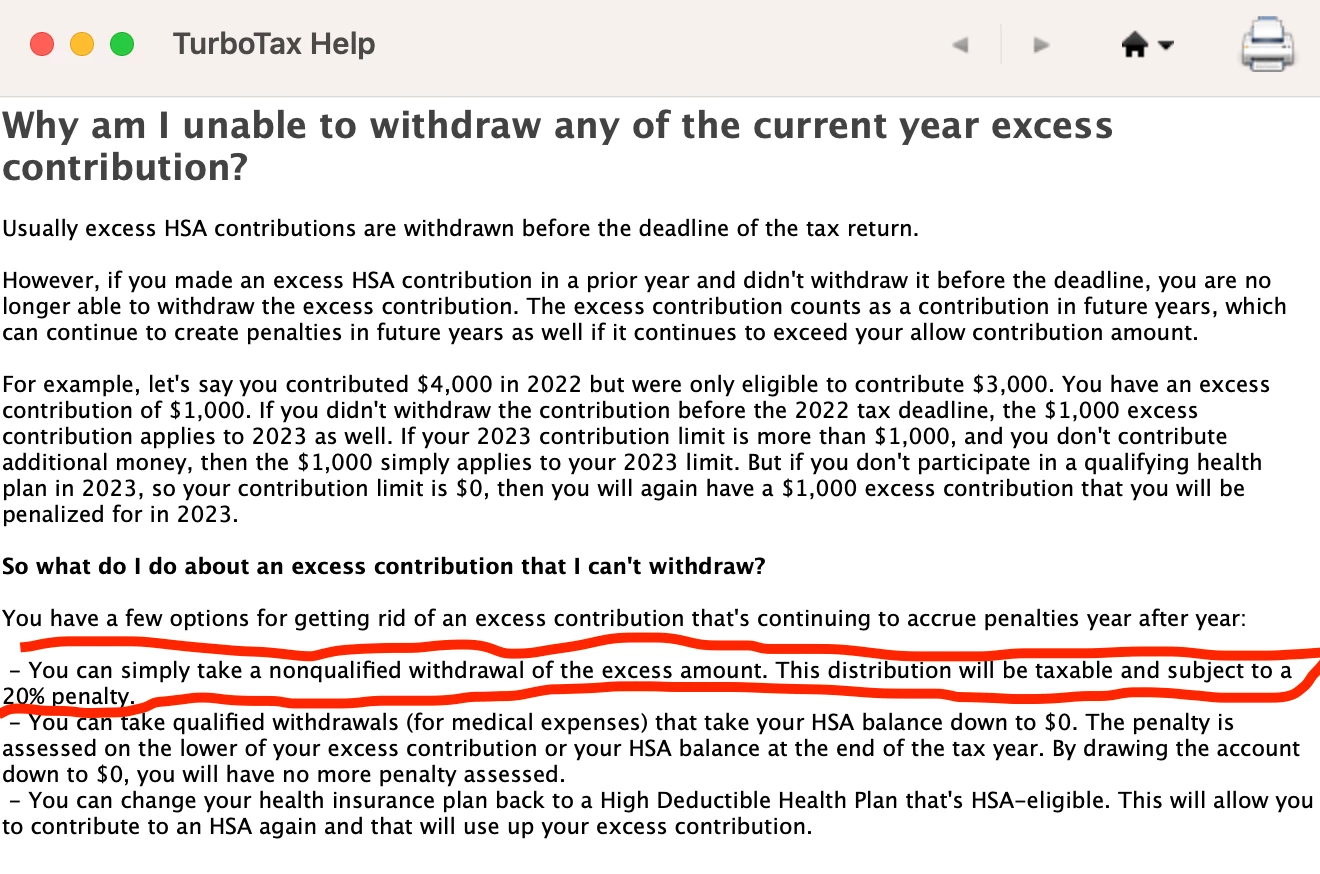

Excess HSA Employer Contribution With Closed HSA Account

Background. On my wife's W2 for 2022 there's $358 "W" employer HSA contribution in box 12. Of them $54 were in excess. That excess wasn't withdrawn yet. Back then my wife had 2 HSA accounts (one with no contributions in 2022 from previous employer). After marring in January 2022, my wife wasn't eligible for HSA anymore, and moved from high deductible to shared deductible health plan. So excess contribution happened in Jan 2022. In 2023 funds in the HSA account that got excess contributions ran out because of service fees every month, and account got closed. 1099-SA wasn't provided for 2023 for that HSA account since there were no contributions, or distributions, only service fees. Another HSA account from previous employer is still open with >$54, and 1099-SA was provided for it (I think because of distributions).

Problem. When filing taxes for 2023, Turbotax now keeps asking in the loop if my wife had high deductible in 2023 / Dec 2022, and I keep answering "no". I cannot file because of that.

Question. It's my understanding that we need to reach out to HSA account provider asking to withdraw excess contribution in order to resolve this issue. But since the HAS account was closed in 2023, it doesn't make sense to me. So what should we do to file this year? Since account is closed, is amount considered withdrawn? If so, how can we report it in Turbotax? Should we reach out to HSA provider to withdraw anyway? If so, which one? Should I ask for IRS extension at this point?

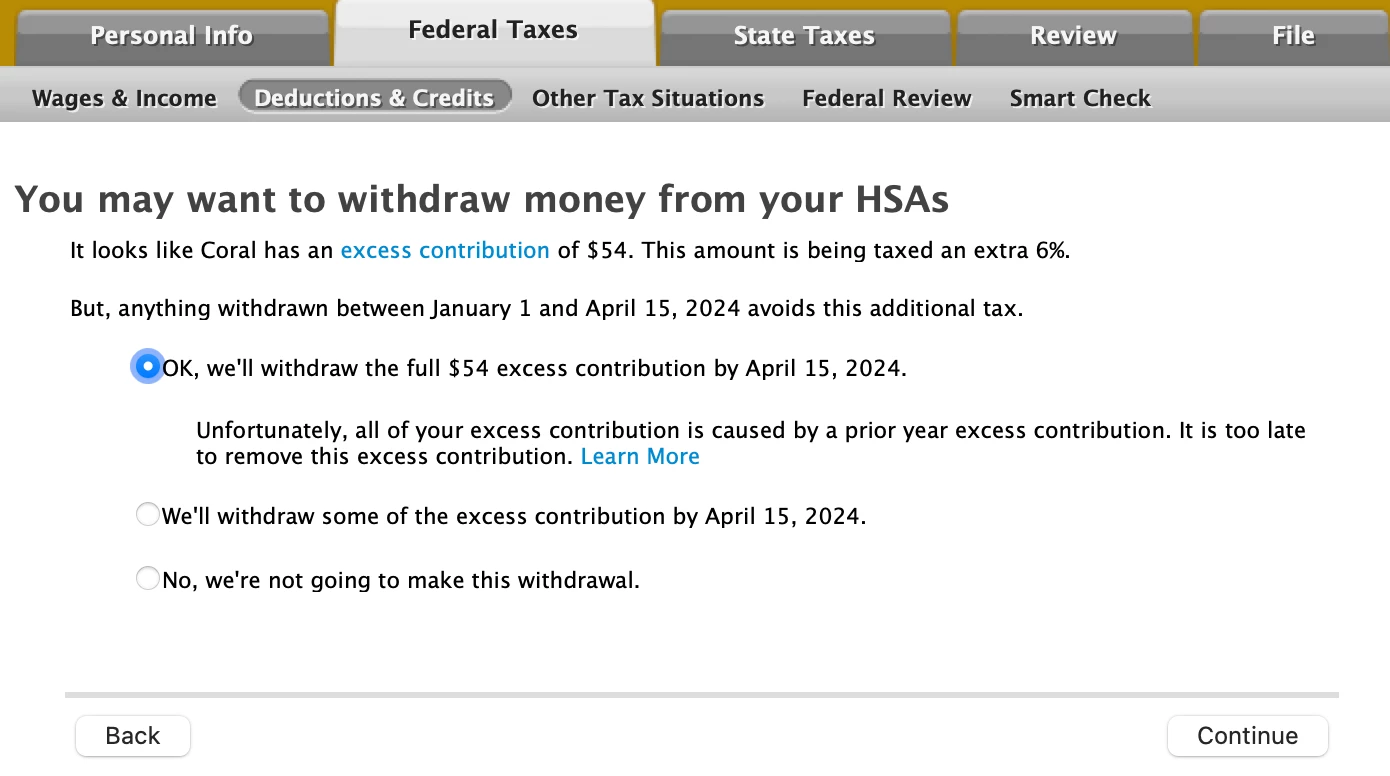

But how will I report the non-qualifying withdrawal in Turbotax 2023? I don't know which options to choose below.

But how will I report the non-qualifying withdrawal in Turbotax 2023? I don't know which options to choose below. 1a) Should I choose option 1 above because we are withdrawing the amount of excess contribution, just as non-qualifying purchase?

1a) Should I choose option 1 above because we are withdrawing the amount of excess contribution, just as non-qualifying purchase?