How do I force Turbotax to divide mortgage interest and property tax for first year rental converted from personal use

The situation I have:

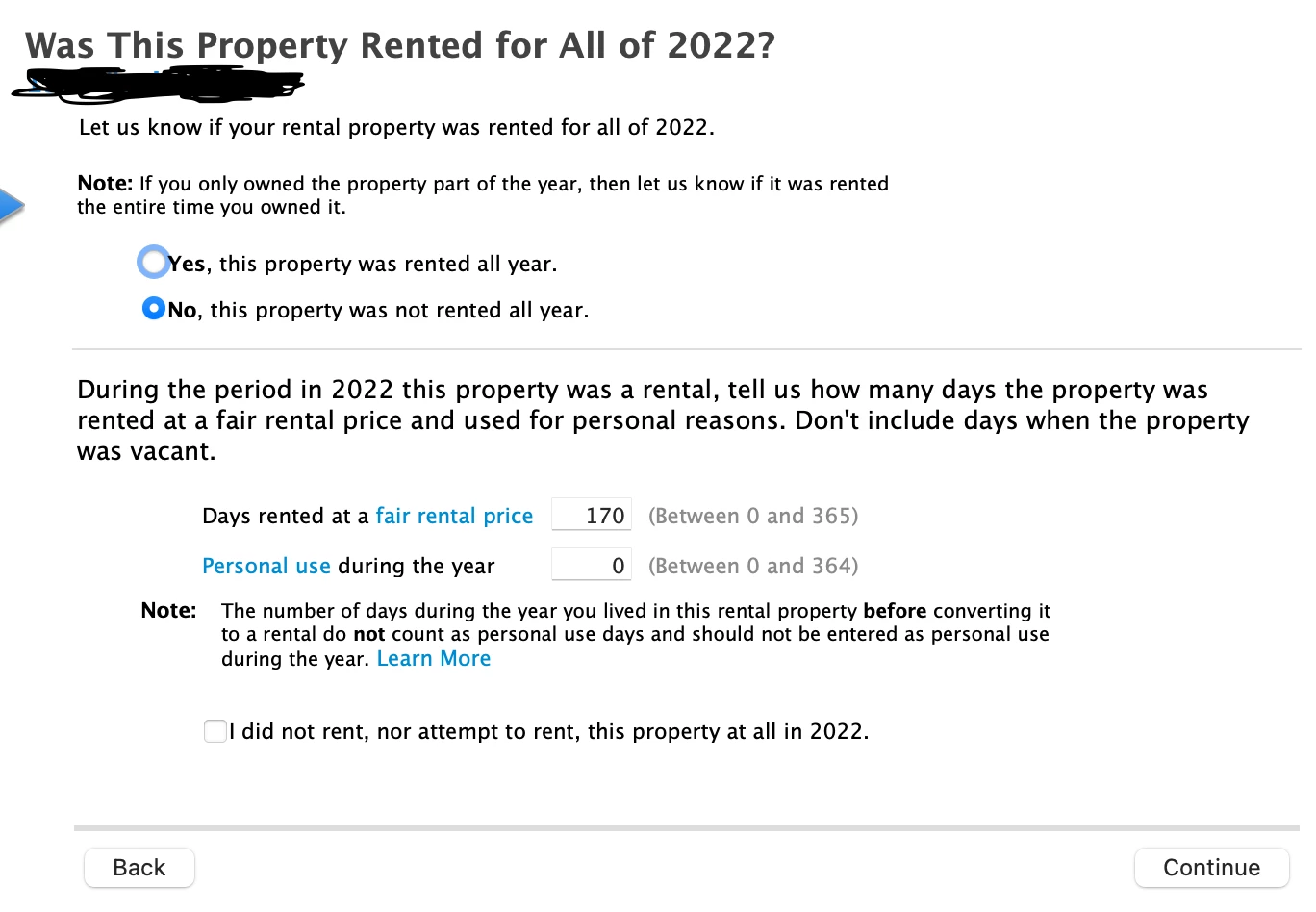

In 2022, I bought a new house B and moved from my old house A on 6/1. I put house A online and got the tenants on 7/15 who have rented since then. House B became my primary residence, and house A was converted from personal use to a rental property. I believe I will get divided mortgage interest and property tax for schedule A and E. However, turbotax doesn't allow me. Specifically it's the following restriction on personal use days in the interview flow:

It clearly said that "The number of days during the year you lived in this rental property before converting it to a rental do not count as personal use days and should not be entered as personal use during the year."

Therefore, I put 0 for personal use. That means TurboTax will not be able to divide my mortgage interest and property tax based on rented days and personal days, which I confirmed by checking the schedule A and schedule E. Does anyone have the same issue when they become landlord for the first time and need to fill schedule A and E correctly?

The closest answer I found is this post, but I don't believe it gave the correct answer. Firstly, I think the statement in the answer is wrong: "Make sure you said it 'was rented all year' (which means all year after available for rent).". If you selected "was rented all year", you won't even be able to see the options for rented days and personal use days. Secondly, the note on the screen clearly says the days living in this property before conversion does NOT count as personal use days, and the answer in that post still did that just trying to have turbotax make the split.

Thanks in advance.