If the property was vacant because you had no tenants it would still be rental property until the day it was sold. It is not necessary to enter income or expenses if there are none.

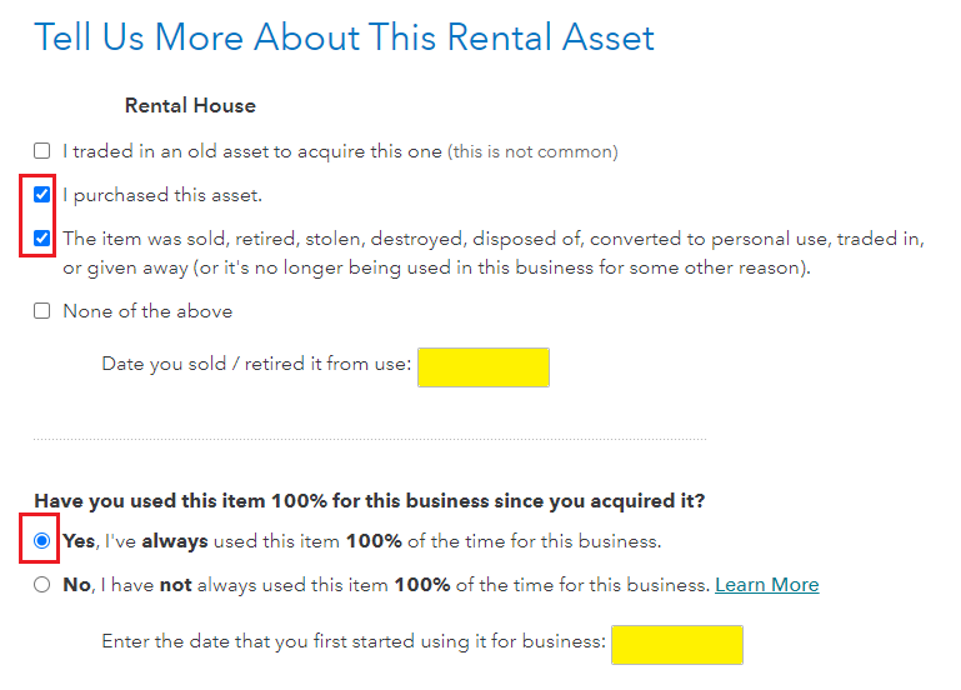

To report the sale you would indicate the property was purchased and also sold, retired, ...... etc. Next you would select 'Yes' it was always used 100% of the time for business (this assumes there was no personal use of the home before the sale). Enter the date of sale and then TurboTax will ask you about the sale, including sales price, selling expenses, etc. It will allow depreciation up to the date of sale and would include that as part of the sales process for any gain on the sale. See the image below.

Depreciation is recaptured at the time of sale and is taxable at a maximum 25% tax rate up to the amount of gain. If there is gain in excess of the depreciation claimed the excess will be taxed at a maximum rate of 20% if it was held long term (more than one year).

Please update here is you have more questions.