Dave,

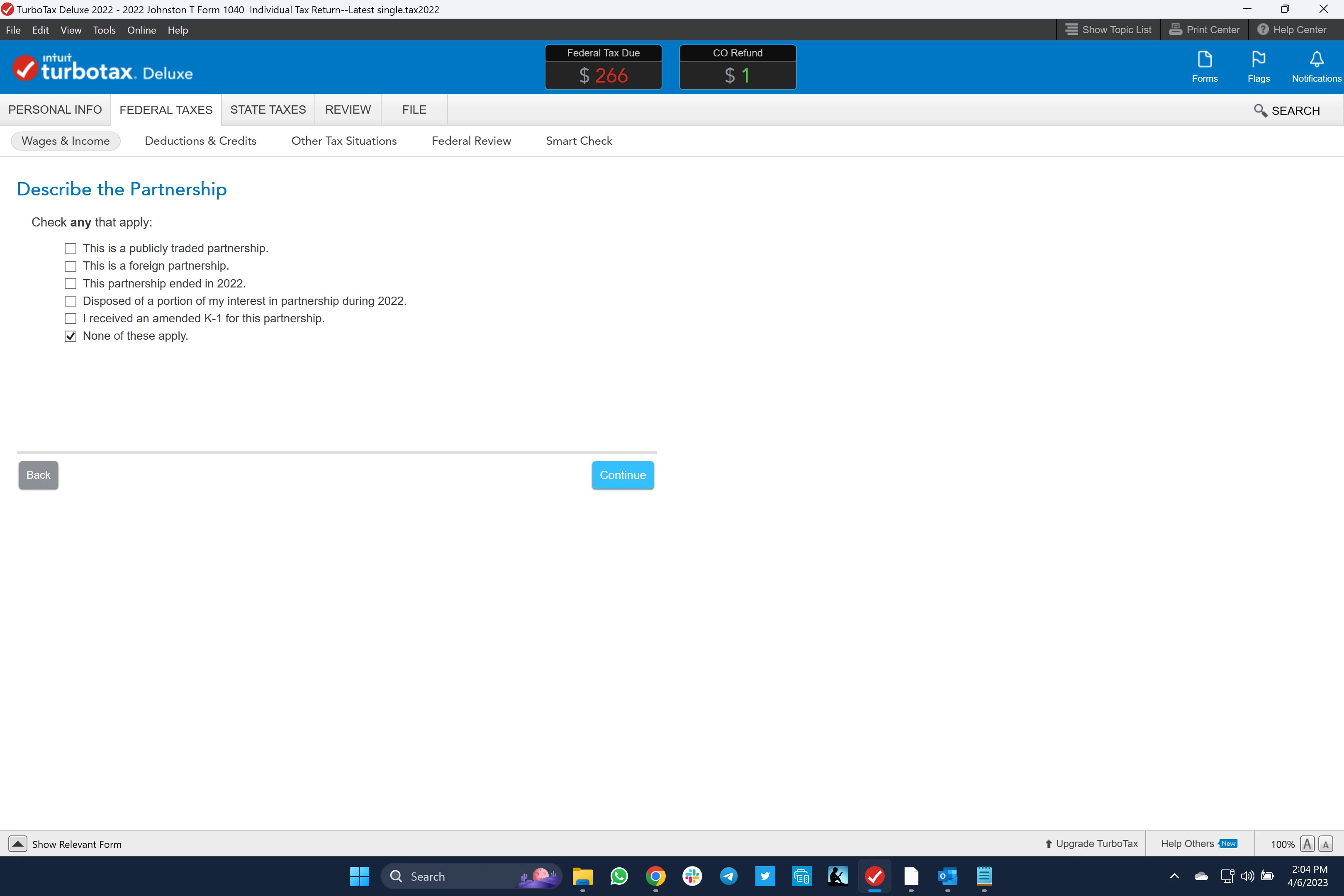

The more I think about this, I'm thinking that possibley I shouldn't report a capital gain at all. See this screenshot:.

The partnership didn't end, nor did I "dispose of a portion of my interest in the partnership" itself. Yes, I got a payout from the partnership for the sale of the asset owned, but I didn't actually sell a portion of the partnership itself. I'm thinking I would just adjust my tax basis to reflect the rent payment distributions as well as the distribution of the gain on the asset itself. But I welcome your thoughts if I'm going astray here. Tx!

@Rick19744, I've seen your comments as well on K1 questions. I welcome your take on the above issue if you have time and a willingness. Thanks.

Here are my comments on this situation:

- K-1's don't technically have anywhere to reflect that they are "disposed". You either receive a normal K-1 or you receive a final K-1; or it could be an amended K-1 should something have changed.

- Since you indicate your K-1 is not marked final, this is just a normal K-1.

- You input the information on the K-1 into TT as you would any other year, AND you do not indicate in TT that this is a final K-1.

- Based on your facts, you also did not dispose of any of your partnership interest. The partnership just sold an asset and is reporting any gain along with any other activity from the partnership.

- A partner is responsible for maintaining their tax basis in their partnership interest. Hopefully you have maintained this as this is a critical component in partnership tax.

- Your tax basis begins with your capital investment and is adjusted each year by the applicable lines on the K-1

- While the current K-1 reflects "tax capital" in box L, this is not, in general, the same as your tax basis.

- You also need to update your tax basis schedule for the applicable lines on the current year K-1.

- After updating your tax basis for the applicable lines on the K-1, if your tax basis goes negative, you have a capital gain that needs to be reported separately. Tax basis cannot go below zero.

- Essentially, if your tax basis goes negative, this negative amount is reported on form 8949 which will then flow to schedule D. Doing this means your tax basis is now zero.