Positive ending capital account and final K-1 box 1 not matching distribution in 19A

Hi,

I received a K-1 marked as final and amended and see below numbers. I am little lost on calculating below section since the K-1 is marked as final.

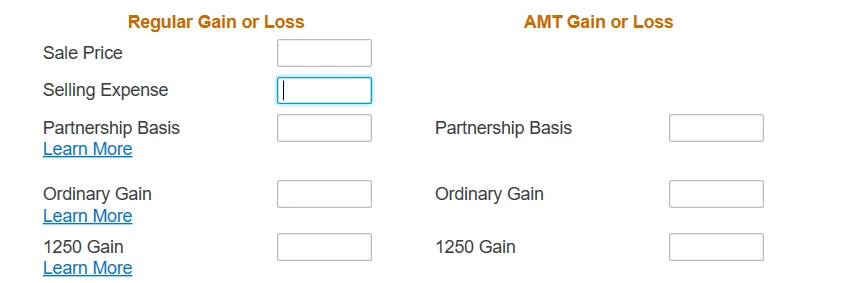

Sale price -- not in the K-1

Sale Expense -- not in the K-1

Partnership Basis -- no supporting document in the K-1 to calculate this as well

Ordinary Gain -- not sure what to enter here

1250 gain -- I see this number as 3735 in Box 9c

Other amounts in the K-1:

Box 1: 8945 - but my distribution including the initial investment is nowhere close to this(initial investment was 2000)

Box 5 interest income: 104

Box 9c: 3735

Box 10: 11078

Box 19 A: 5490

Box 20 A: 104

Box 20 N: 54

Box L numbers:

Opening capital account: -7250

Current year net income(loss): 20321

Withdrawals and distributions: 5490

Ending capital account: 7579

I selected 'This partnership ended in 2023' and 'received amended K-1 for this partnership'

Describe partnership Disposal: Complete Disposition

What type of disposition was this: Sold partnership interest

Entered purchase and sale dates(2016 to 2023)

Can someone please help me how to enter the sale info section and anything else I need to be aware of?

Thanks