It depends. There will be a recapture of the depreciation expense for the rental period.

If the home is currently set up as a rental on your return at the time of sale, then you need to complete the sale in the rental asset or assets.

- Search > Type rentals > Click the Jump to.. link > Edit beside the rental and select Update beside Assets

You will need to answer "No" to Special Handling to answer the questions about using it as a home On the next screen you will be asked 'Was this asset included in the sale of your main home?'. Select Yes and then follow the screens to finish the reporting of your sale. You will need to count the number of days it was used as a rental.

TurboTax will allocate the proper taxable amount due to the depreciation from the gain on the sale, only gain that exceeds this will be eligible for the exclusion. You will not see 100% of the gain excluded, even if the total gain is below $500,000 for married taxpayers.

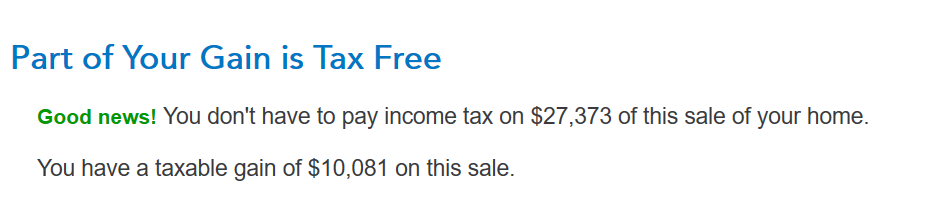

Most of your gain will be excluded but you will have some taxable gain for the period it was rented. TurboTax will show you the excluded and taxable gain. See the image below from my example.