Solved

Sale of rental property that was primary residence

I am using Turbo Tax Premier on Desktop (Windows). I need help in reporting the sale of rental property in 2021. Here are the details:

- Bought the single family home (property 1) as primary property in 2006 for $400,000

- Lived in the property (primary residence) through 2013.

- Bought a new primary residence in 2013. Put the previous house (property 1) for rent in 2013. FMV at the time of rental conversion was $325,000

- Sold property 1 (now rental property) in 2021 for $500,000.

- Closing costs were $30,000 and additional required updates were $26,000

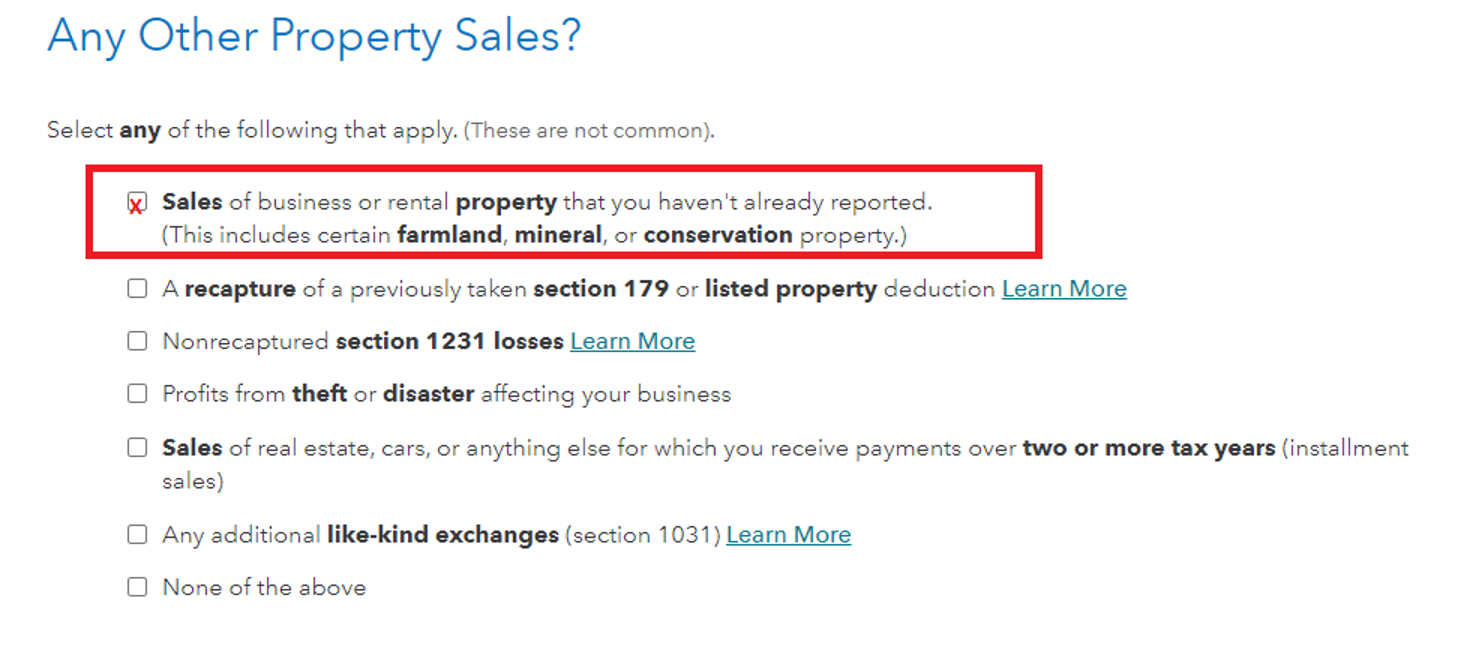

I need help in TurboTax to report this sale of rental property. Could someone tell me where do I need to show this sale? Looking at similar questions on this community forums, I see some people recommending reporting the sale in the rental section using the asset and sale of property/depreciation section OR using the Sale of Business Property section.

I'd highly appreciate if someone walks me through the steps to show this sale of rental property.