Question

Which rental expenses are pro-rated?

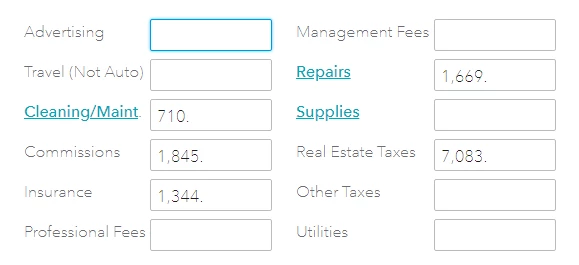

I converted my primary residence to a rental property in the middle of 2018. I have my all of my receipts for expenses. When I enter them into TurboTax, it is doing some pro-ration based on the date I put the rental in service that is not matching up with my hand calculations. I cannot see the math that TurboTax is doing so it is hard to understand the error.

Of the following fields, which ones will TurboTax pro-rate based on the date I put it in service? Which ones are includes as expenses at 100%?

Thanks,

Sal